As oil prices continue to fall to around $40 a barrel, many oil-dependent nations are seeing their main source of profit drying up. One particularly frightening report from the International Monetary Fund stated that most Middle Eastern countries could run out of money in just five years. But the oil-rich Middle East has spent significant wealth on trying to find new sources of income once the petroleum economy becomes unprofitable. Some countries have already begun to shift their economies away from oil production. So, can the Middle East survive without oil?

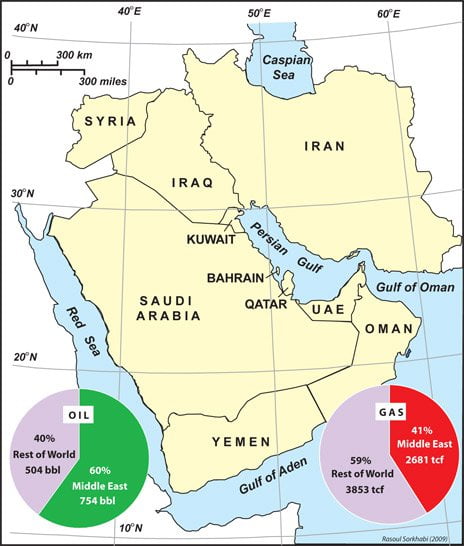

Well, the majority of the Middle East’s oil comes from just six countries. Iran, Iraq, Kuwait, Qatar, Saudi Arabia, and the United Arab Emirates produce more than 25 million barrels a day. But despite the region’s oil heavy focus, the country of Bahrain has already become their first post-oil economy. Bahrain stands as a model for other countries, as they’ve never had much oil to boost the economy. There is instead an emphasis on banking, tourism, manufacturing, and construction. In fact, Bahrain is a main financial center for all the surrounding oil money, and their success is partially due to a unique niche: Islamic banking.

Islamic or halal banking, is simply banking that follows sharia law, and for many religious people in the Middle East, it is a necessity. In particular it prevents usury, or the charging of excessive interest on loans, which is prohibited in the Quran. It also does not allow investment in things like pork, alcohol, or tobacco, as those too are prohibited. The demand for this sort of specific care has led to significant financial growth for Bahrain and other countries like the United Arab Emirates. Saudi Arabia, which still sees around three-quarters of their revenue from oil, has begun to diversify the output and works to export minerals like aluminum and gold to eventually replace oil. Additionally, many Middle Eastern powers are investing in alternative energies. Saudi Arabia is already setting itself up to provide solar and nuclear power to the entire Gulf Coast.

And while all these countries are looking for lucrative income replacement, the richest of the rich are actually investing in other countries. Qatar, which has the highest GDP per capita in the world, recently promised to invest $15 billion dollars in Asia, with about $200 million dollars worth of property purchases in India alone. But since the Middle East has spent much of the 20th century raking in oil wealth, there is considerably worry about the future for the youth. As extremely high paying oil jobs transition into a more transit, financial, and service industry many fear that oil-funded government programs will end.

Saudi Arabia provides free education and healthcare, with no taxation. So even if those rich countries can jumpstart alternative revenue sources, young residents will likely have less job security, fewer social benefits, and they’ll have to work much harder than the current generation. And before a post-oil economy arrives, there’s no guarantee that Saudi Arabia will have enough reserves to make it there.