There is a standard and well-worn process to getting business loans. Determining what you need the loan for and how much you need. Choosing the right business loan for your needs. Finding a lender, preparing your paperwork and, finally, qualifying for the loan.

There is a standard and well-worn process to getting business loans. Determining what you need the loan for and how much you need. Choosing the right business loan for your needs. Finding a lender, preparing your paperwork and, finally, qualifying for the loan.

The process, although time-consuming and often frustrating, is simple enough. The first difficult decision you must make is determining the type of loan that best resolves what you need a loan for and how much you need.

What you need to know

Ask yourself why you need the money, then how long will it take to pay it back and, finally, do you have a way to secure the loan. The answers to those questions will determine the kind of loan you need.

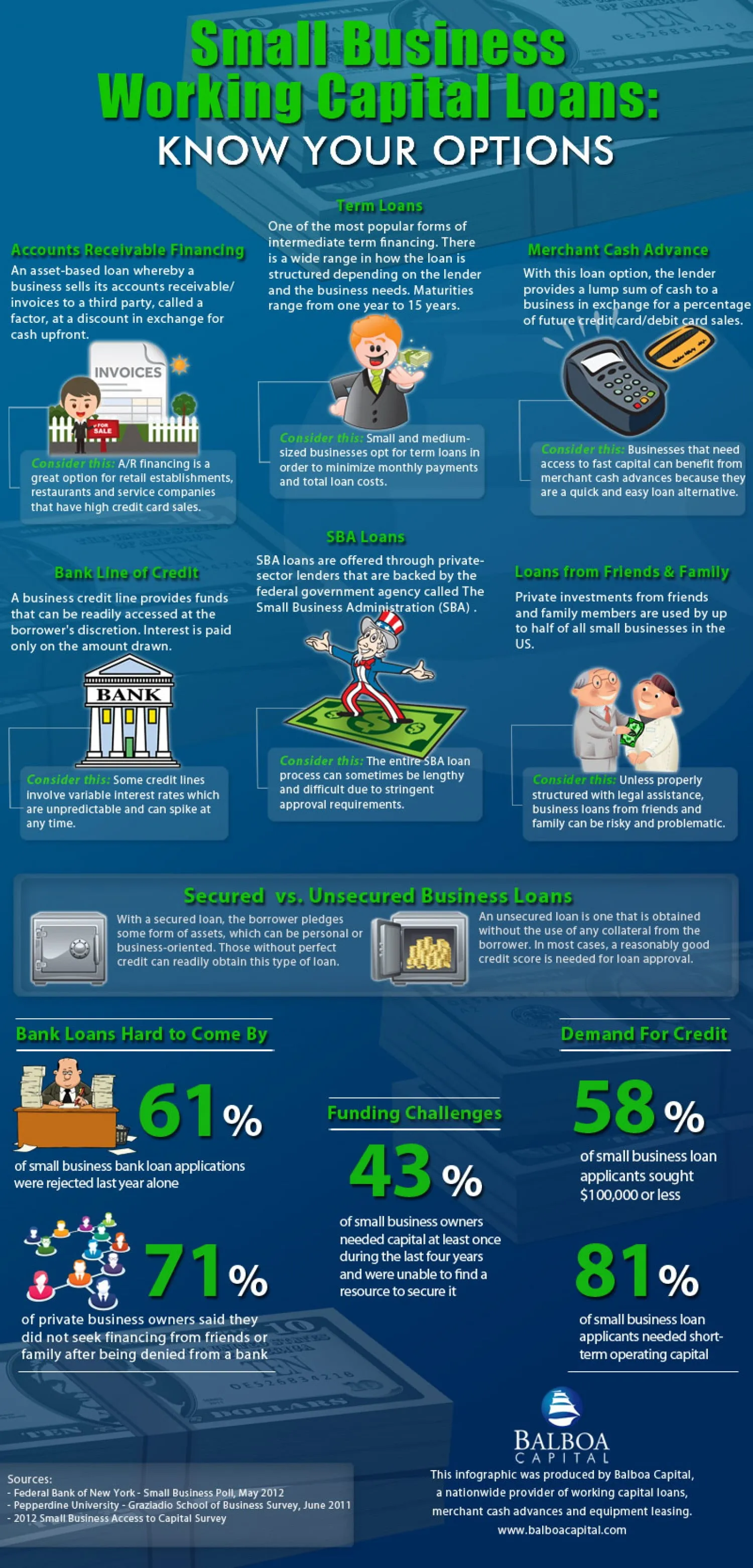

According to smallbusinessloans.co, the most common types of business loans include:

- Line of credit. The most common, and often the most useful, type of loan you can get from a bank, a line of credit gives your business access to capital on an “at need” basis. There will be a cap on the amount you can access, but it is useful for managing cash flow and for dealing with unexpected expenses. A line of credit can be used for almost any business purpose and as long as it is paid, your business should have no trouble renewing it on whatever basis decided between you and the bank.

- Accounts receivable financing. If your bank is hesitant about giving you an unsecured line of credit, accounts receivable financing might make it easier and more palatable for them. This credit is secured by the money due to your accounts receivable department.

- Term loans. Term loans are what most people think of when they are considering a loan. They have set amount of money borrowed, they have a set payment schedule and interest is paid on the principal. Term loans for a business, however, are usually set up for a shorter duration than personal loans with higher payments or a balloon payment due at the end of the loan term. Although good for one-time investments and business expansions, they are not particularly flexible.

- Working capital loans. These loans borrow against the profits of the company to generate operating capital. They are commonly used by seasonal businesses or ones that have large fluctuations in profit and expenses. Working capital loans tend to be relatively modest with short terms.

- SBA small business loans. SBA loans are usually term loans but with lower interest rates. These loans are guaranteed by the United States government and, although difficult and time consuming to apply for and receive, are very attractive to banks. The Small Business Administration tracks the 100 most active lenders for these types of loans.

Although these loans have similarities, the differences are important when the time time to borrow the money comes. Knowing what type of loan you want and need will make the borrowing process considerably easier for the borrower and quicker for the lender to give you an answer.

Although going through familiar banks is the most common method of borrowing money for your business, online financing options exist to help business owners get operating capital or borrow money for expansion and other needs. No matter what type of loan you are looking for or where you intend to get it, the paperwork is very similar for all types of business loans except for Small Business Administration loans.

The paperwork for SBA loans is more detailed and thorough. Starting with SBA loan paperwork can make it more likely that your loan applications will go smoother through your local bank or online. Having filled out the most detailed application, completing others will be much simpler and quicker.

Other options?